All Categories

Featured

Table of Contents

- – What are the tax implications of an Income Pro...

- – What are the tax implications of an Annuity Co...

- – What should I look for in an Guaranteed Retur...

- – Who offers flexible Senior Annuities policies?

- – Is there a budget-friendly Annuities option?

- – How do I get started with an Tax-deferred An...

Note, however, that this doesn't state anything about adjusting for inflation. On the plus side, even if you think your choice would be to buy the stock exchange for those 7 years, which you 'd obtain a 10 percent annual return (which is far from certain, specifically in the coming decade), this $8208 a year would certainly be more than 4 percent of the resulting nominal stock worth.

Instance of a single-premium deferred annuity (with a 25-year deferral), with 4 payment choices. The month-to-month payout here is greatest for the "joint-life-only" alternative, at $1258 (164 percent greater than with the instant annuity).

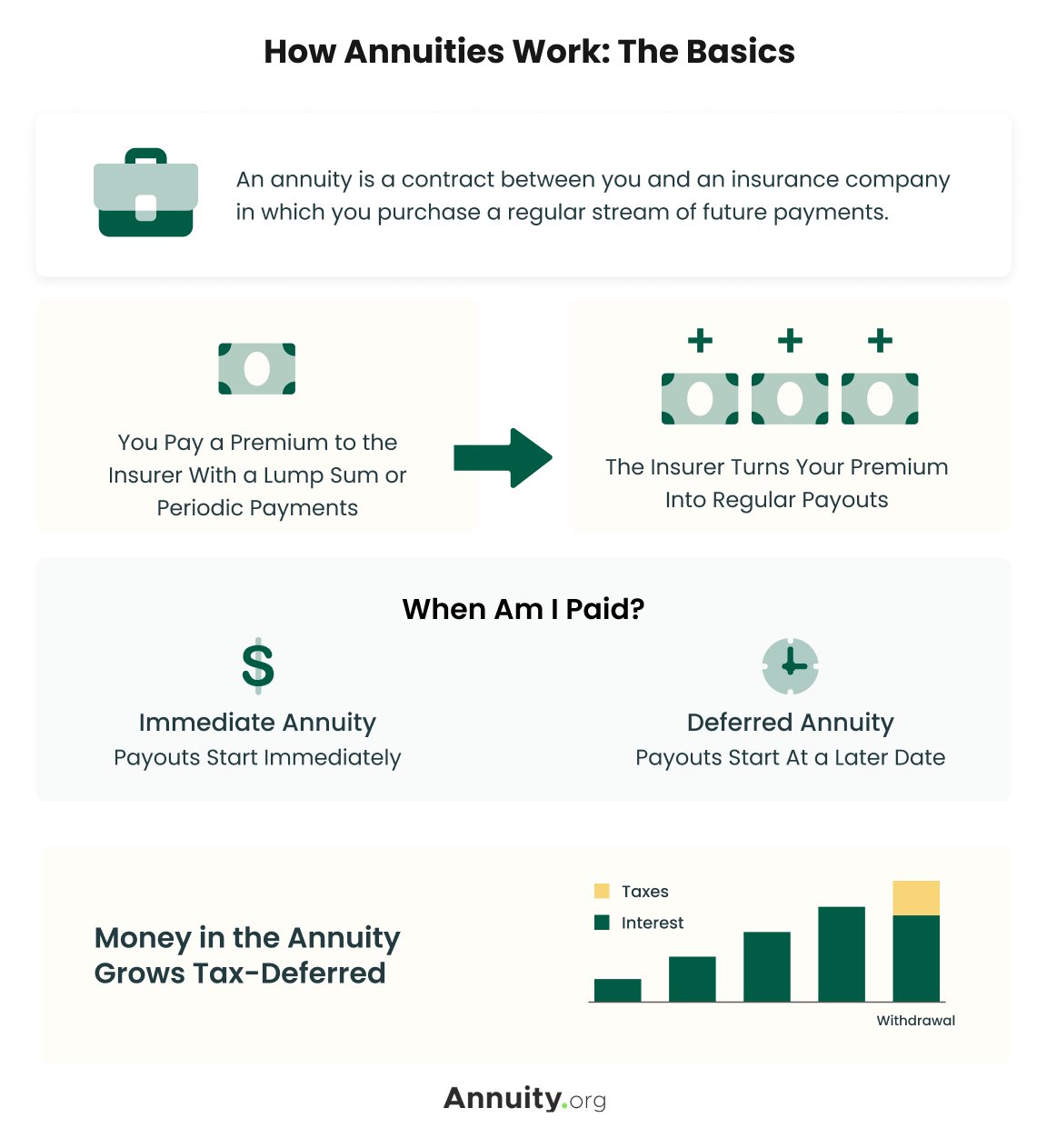

The means you get the annuity will certainly establish the solution to that inquiry. If you acquire an annuity with pre-tax bucks, your costs decreases your gross income for that year. Nonetheless, eventual payments (monthly and/or lump amount) are tired as regular earnings in the year they're paid. The advantage right here is that the annuity may let you defer taxes beyond the IRS payment restrictions on IRAs and 401(k) plans.

According to , getting an annuity inside a Roth strategy results in tax-free payments. Buying an annuity with after-tax dollars beyond a Roth results in paying no tax obligation on the section of each repayment credited to the original premium(s), but the remaining section is taxable. If you're establishing up an annuity that starts paying prior to you're 59 years of ages, you may need to pay 10 percent very early withdrawal charges to the IRS.

What are the tax implications of an Income Protection Annuities?

The advisor's very first step was to establish a comprehensive monetary strategy for you, and after that clarify (a) exactly how the proposed annuity matches your total plan, (b) what alternatives s/he thought about, and (c) exactly how such options would or would certainly not have led to reduced or higher compensation for the consultant, and (d) why the annuity is the remarkable choice for you. - Annuity withdrawal options

Of training course, a consultant may try pressing annuities also if they're not the most effective fit for your scenario and objectives. The factor could be as benign as it is the only product they market, so they fall victim to the typical, "If all you have in your toolbox is a hammer, pretty soon everything begins appearing like a nail." While the expert in this circumstance may not be unethical, it boosts the risk that an annuity is an inadequate selection for you.

What are the tax implications of an Annuity Contracts?

Because annuities frequently pay the agent selling them a lot higher compensations than what s/he would certainly receive for spending your cash in shared funds - Long-term care annuities, let alone the absolutely no compensations s/he would certainly obtain if you purchase no-load mutual funds, there is a big reward for representatives to push annuities, and the more complex the much better ()

An unscrupulous advisor suggests rolling that amount into brand-new "better" funds that just happen to lug a 4 percent sales tons. Agree to this, and the consultant pockets $20,000 of your $500,000, and the funds aren't most likely to execute better (unless you chose much more improperly to begin with). In the exact same example, the expert might guide you to purchase a complicated annuity with that $500,000, one that pays him or her an 8 percent commission.

The advisor tries to rush your choice, claiming the offer will quickly go away. It may undoubtedly, yet there will likely be similar deals later on. The advisor hasn't identified just how annuity settlements will certainly be tired. The consultant hasn't disclosed his/her compensation and/or the charges you'll be charged and/or hasn't revealed you the effect of those on your eventual payments, and/or the settlement and/or charges are unacceptably high.

Your household history and existing wellness factor to a lower-than-average life span (Annuities for retirement planning). Current passion prices, and hence projected payments, are traditionally low. Even if an annuity is best for you, do your due persistance in comparing annuities offered by brokers vs. no-load ones marketed by the releasing business. The latter may require you to do more of your own study, or use a fee-based financial expert that might receive settlement for sending you to the annuity provider, but might not be paid a greater compensation than for various other investment alternatives.

What should I look for in an Guaranteed Return Annuities plan?

The stream of regular monthly repayments from Social Safety resembles those of a deferred annuity. As a matter of fact, a 2017 relative analysis made an extensive comparison. The adhering to are a few of one of the most salient factors. Given that annuities are voluntary, individuals buying them typically self-select as having a longer-than-average life span.

Social Protection benefits are fully indexed to the CPI, while annuities either have no rising cost of living protection or at a lot of supply a set portion annual rise that might or may not make up for inflation completely. This kind of biker, similar to anything else that enhances the insurance provider's risk, needs you to pay even more for the annuity, or accept lower settlements.

Who offers flexible Senior Annuities policies?

Disclaimer: This write-up is planned for informational purposes only, and ought to not be taken into consideration economic advice. You need to consult a monetary specialist prior to making any significant economic choices. My job has had lots of unpredictable weave. A MSc in theoretical physics, PhD in experimental high-energy physics, postdoc in bit detector R&D, research position in speculative cosmic-ray physics (consisting of a couple of sees to Antarctica), a quick job at a small engineering solutions company supporting NASA, followed by beginning my very own tiny consulting method sustaining NASA jobs and programs.

Considering that annuities are planned for retired life, taxes and penalties may apply. Principal Protection of Fixed Annuities. Never shed principal as a result of market efficiency as repaired annuities are not invested in the marketplace. Even throughout market slumps, your money will not be influenced and you will certainly not lose cash. Diverse Financial Investment Options.

Immediate annuities. Used by those that desire trusted revenue quickly (or within one year of purchase). With it, you can customize income to fit your demands and develop income that lasts forever. Deferred annuities: For those who wish to grow their cash with time, but want to delay accessibility to the money up until retirement years.

Is there a budget-friendly Annuities option?

Variable annuities: Offers higher potential for development by investing your money in investment choices you pick and the ability to rebalance your portfolio based on your choices and in a manner that straightens with transforming financial goals. With taken care of annuities, the firm spends the funds and provides a rate of interest to the customer.

When a fatality case accompanies an annuity, it is very important to have a called beneficiary in the contract. Various options exist for annuity survivor benefit, depending upon the contract and insurance company. Choosing a reimbursement or "duration particular" alternative in your annuity offers a fatality benefit if you die early.

How do I get started with an Tax-deferred Annuities?

Naming a recipient various other than the estate can help this procedure go extra smoothly, and can help make certain that the proceeds go to whoever the individual desired the cash to go to rather than going through probate. When existing, a fatality benefit is automatically included with your agreement.

{kind=link}

Table of Contents

- – What are the tax implications of an Income Pro...

- – What are the tax implications of an Annuity Co...

- – What should I look for in an Guaranteed Retur...

- – Who offers flexible Senior Annuities policies?

- – Is there a budget-friendly Annuities option?

- – How do I get started with an Tax-deferred An...

Latest Posts

Analyzing Annuity Fixed Vs Variable Everything You Need to Know About Financial Strategies Defining Variable Annuity Vs Fixed Annuity Advantages and Disadvantages of Fixed Indexed Annuity Vs Market-va

Decoding Tax Benefits Of Fixed Vs Variable Annuities A Comprehensive Guide to Investment Choices What Is Fixed Vs Variable Annuity? Features of Smart Investment Choices Why Fixed Annuity Vs Equity-lin

Highlighting the Key Features of Long-Term Investments Key Insights on Variable Vs Fixed Annuity What Is the Best Retirement Option? Benefits of Fixed Income Annuity Vs Variable Growth Annuity Why Cho

More

Latest Posts